- Home

- China

- World

- Europe

- Politics

- Business

- Opinions

- Tech & Sci

- Culture

- Sports

- Travel

- Nature

- Picture

- Video

- Live

- TV

- Specials

Share

Copied

A huge advertisement for Bitcoin is displayed near Shibuya train station in Tokyo, Japan. (Credit: ASSOCIATED PRESS)

Central banks have been wary of cryptocurrencies as long as they have existed. Bitcoin and its many rivals operate far from the reach of financial regulators, their inventors are invariably anonymous and often emerge from fringe political or hacking communities.

The banks were right to be worried – the development of cryptocurrencies was and is revolutionary, their use of an open-source, peer-to-peer technology – blockchain – has disrupted financial markets without any oversight from states or their once all-powerful central banks.

In response to the threat, some nations are developing their own central bank-issued digital currencies (CBDCs) that would counteract the dangers from decentralized rivals.

Unlike cryptocurrencies, CBDCs are regulated by the issuer, carry a solvency guarantee and can be used to identify fraudulent and illegal transactions. A CBDC unit represents fiat money – legal tender, acting as a secure digital equivalent of a paper note or coin.

A user on a Robocoin kiosk selling/buying Bitcoins (Credit: AP)

China throws its hat into the ring

China now looks set to become the first of the world's major economies to launch a CBDC, stealing a march on its competitors, be they other nations or multi-national businesses such as Facebook, which is developing its own digital currency – Libra.

A senior official at the People's Bank of China (PBOC) caused much speculation when he told audiences at a China Finance 40 Forum, in Yichun, Heilongjiang, that a Chinese CBDC was "close to being out."

The comments, made by Mu Changchun, a deputy director of the PBOC's payments department, were subsequently pored over by much of the world's financial and business press.

Since then, excitement has mounted although the PBOC governor Yi Gang recently stated there wasn't a "timetable" for its release.

The adoption of a CBDC would mark a significant step forward for China which has spent the past five years researching digital currencies. Until now, Bitcoin has been the dominent player in the cryptocurrency market but China is seeking to change the model.

"Bitcoin catalyzed the creation of an entire cryptocurrency ecosystem," said Valery Vavilov, CEO and co-founder of the Bitfury Group, "it has grown in both market capitalization and popularity. At the same time, digital commerce expanded. These forces brought cryptocurrencies and blockchain to the forefront."

Although financial institutions other than the Chinese central bank are set to be allowed to issue the digital currency, they are expected to have to deposit assets with the equivalent value to any money they issue. This will mean that the volume of funds in circulation will remain effectively capped and mean that the new digital currency acts as a virtual extension of the Yuan rather than a new currency.

China, unlike many other nations, is well set up for a digital currency, as it boasts the world's largest cashless market. A majority of transactions are conducted by scanning QR codes, using mobile payment apps such as Alibaba's Alipay or WeChat, owned by Tencent.

Libra causes a stir

Facebook announced it intends to launch Libra in 2020. (Credit: Thomas Trutschel/Getty)

In terms of digital currencies, scale is everything. The more people who can use the money, the more compelling the case for businesses to accept it and therefore the greater its utility. Few networks can match the scale of the Chinese state, although for sheer numbers of users, Facebook is one. The social media company has announced its intention to launch Libra in 2020.

One of the few networks to rival the Chinese state in terms of number of users, Libra could in theory be accessed by any of Facebook's 2.4 billion users. In typical Silicon Valley fashion, the social network's mission statement expressed a desire to create "a simple global currency and infrastructure that empower billions of people."

The announcement led to widespread consternation from the world's central banks, politicians and regulators, who feared that – far beyond Bitcoin – Libra had the potential to significantly disrupt financial markets and reshape embedded institutions.

Leading the criticism, Jerome Powell, chairman of the US Federal Reserve, warned that its launch should be blocked until Facebook addressed a litany of regulatory concerns, including Libra's susceptibility to money laundering.

Powell's equivalent in the UK, Mark Carney, governor of the Bank of England, argued the world's major banks and financial institutions must have "direct regulatory oversight" over Libra.

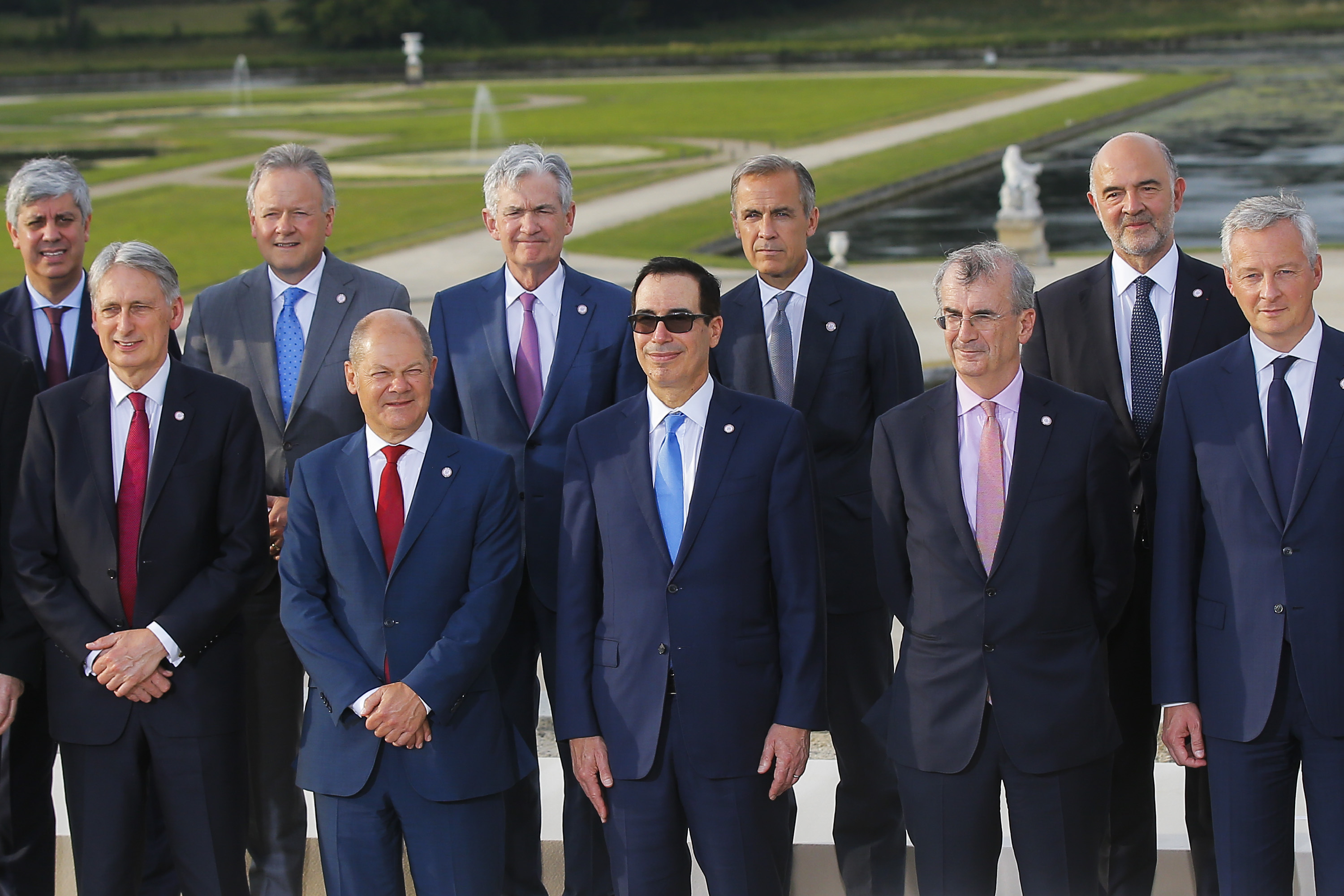

G7 finance ministers and central bankers met in July. The governor of the Bank of England, argued the world's major banks and financial institutions must have 'direct regulatory oversight' over Libra (Credit: AP)

Despite his objections to Libra, Carney is an advocate of digital technology's growing role in finance. During a recent speech at the US Federal Reserve he posited, what he termed a "synthetic hegemonic currency" – a CBDC that could become a global alternative to the US dollar, backed by the world's leading central banks.

"Even if the initial variants of the idea prove wanting, the concept is intriguing," Carney noted.

The Bank of England's governor may be right to seek an international CBDC. The UK faces an uncertain future should digital currencies take off, after access to the EU's blockchain initiative was blocked following 2016's Brexit vote.

Crypto vs the dollar

While Carney's proposal is far from fruition, many smaller countries have already released a CBDC. Nations are turning to crypto for various reasons. Earlier this year the State of Palestine announced it was considering releasing a digital currency as an alternative to the Israeli shekel.

The Marshall Islands, solely reliant on the US Dollar, are set to release their own CBDC later this year, despite previous criticism from the International Monetary Fund (IMF) and the US Treasury Department.

According to a Bank for International Settlements (BIS) report released earlier this year, 70 percent of the world's financial authorities are looking into issuing CBDCs, and two-thirds of them are based in emerging market economies.

Venezuela president Nicolas Maduro oversaw the implementation of the Petro (Credit: Bloomberg/Getty Editorial)

CBDC development has also been prevalent in those countries that have faced censure from Washington. Russia has warmed to the idea of launching a CBDC after being hit with repeated US sanctions, while Venezuela, in an attempt to circumvent sanctions and counteract crippling hyperinflation, launched its CBDC, the Petro, in 2018.

'Security, transparency and trust'

"Many governments see the potential for cryptocurrencies – reduction in costs, more transparency, interoperability, more government control," said Tricia Martinez, a US-based fintech entrepreneur.

Though each CBDC will have its own characteristics, in principle they aim to marry cryptocurrency's convenience and security, with the established characteristics of a conventional banking system, in which money circulation is regulated and backed by a central reserve.

For Bitfury's Vavilov, the benefits of adopting CBDCs "will be the increased ease of state and international operations including trade and fund transfers."

"Cryptocurrencies offer security, transparency and trust by design with no need for complicated validation procedures or third-party checks. They offer simple solutions that save time, make operations easier and more efficient and reduce costs." Vavilov noted.

Control or chaos?

Many other nations remain wary. Japanese banking officials have warned that a digital currency could destabilize their financial system. Across the Sea of Japan, a report from the Bank of Korea (BoK) warned that a CBDC could have detrimental effects – a spike in interest rates as well as a liquidity crunch.

Martinez noted cryptocurrencies could have "adverse impacts for countries. Not all governments have the best intentions and if in the hands of the wrong people, complete transparency and control of a country's digital assets could lead to economic distress and if not worse."

A screen displays the price of bitcoin in Seoul, ROK. (Credit: Associated Press)

Despite reservations remaining about CBDCs, Martinez believes that ultimately the move is a "massive step forward … central banks becoming more open to a centralized cryptocurrency will begin to advance the blockchain and fintech space, opening up regulation and creating more room for innovation."

Her optimism is reflected by Vavilov: "Governments are starting to understand that it is not just a currency, it is a technology that can be used to democratize the way we store and move anything of value more securely, more transparently and much more easily. It is a tool that will improve existing established systems and will build new levels of trust among the people who use those systems".